Medicare in 2026: 5 Rules That Could Cost Retirees Thousands

Medicare is not the simple safety net many retirees expect it to be.

Behind the red, white, and blue card is a complicated system of hospital classifications, income look-back rules, prior authorization requirements, prescription drug limits, plan documents, and benefit restrictions. These rules do not always depend on how long you worked, how much you paid into the system, or how good your plan looks on paper.

In 2026, several Medicare rules and cost traps are affecting retirees in real ways. Some are new. Some are long-standing rules that still catch families by surprise. Either way, most people do not learn about them until a bill arrives.

Here are five Medicare issues every retiree should understand now.

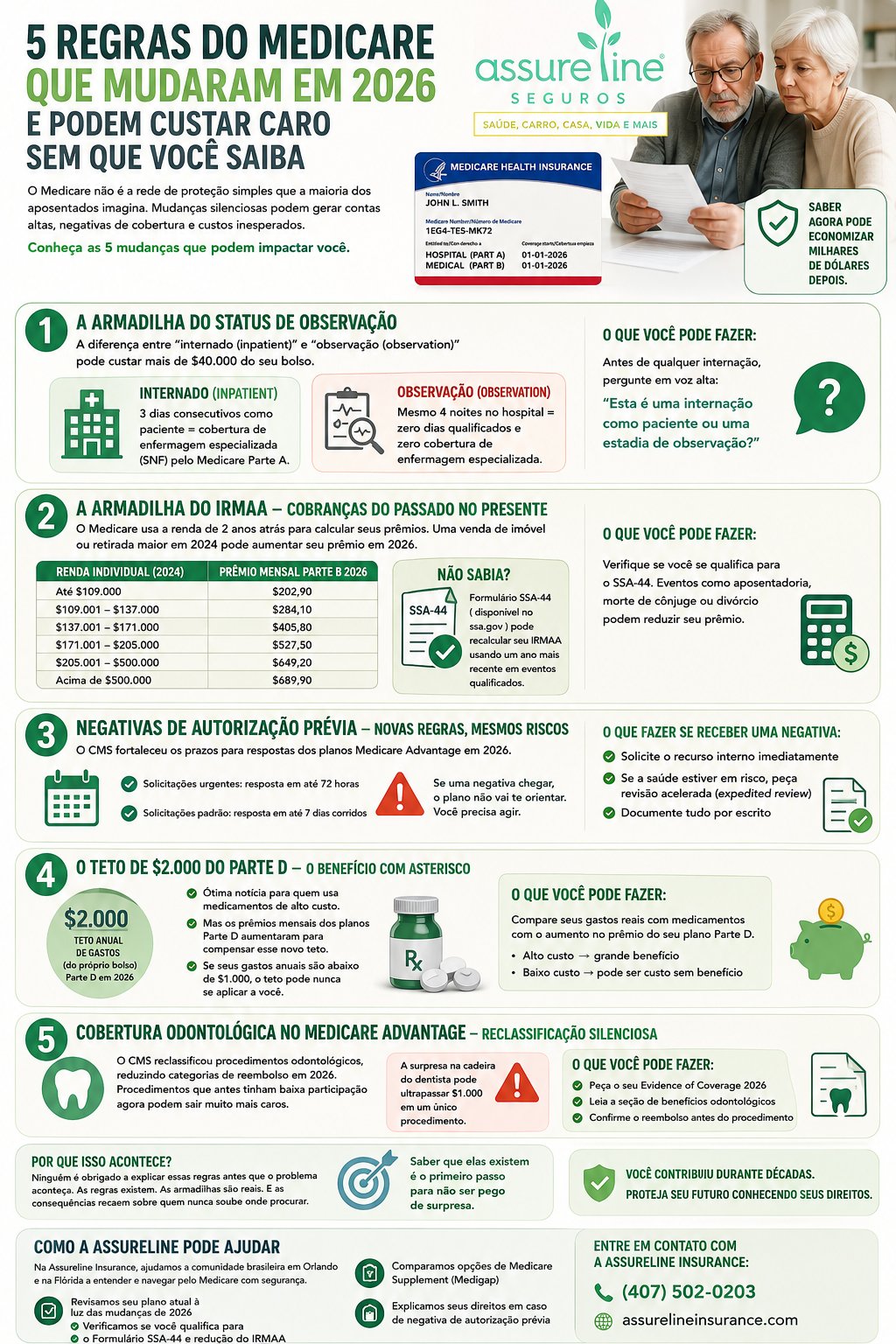

Rule 1: The Observation Status Trap

This may be the most expensive Medicare misunderstanding.

When you are in the hospital, your status matters. You may be classified as an inpatient, or you may be considered an outpatient receiving observation services. To most people, those two situations look exactly the same. You may be in a hospital bed, wearing a wristband, receiving medication, seeing doctors, and staying overnight.

But for Medicare billing, the difference can be enormous.

Under Original Medicare, Part A generally covers skilled nursing facility care only after a qualifying inpatient hospital stay of at least three consecutive days. Time spent in the emergency room or under observation does not count toward that three-day requirement, even if you stay overnight. Medicare also makes clear that a person can spend the night in the hospital and still be considered an outpatient.

That means a patient can spend several nights in the hospital, get discharged to a skilled nursing facility, and later find out Medicare will not cover the facility stay because the hospital record never showed a qualifying inpatient admission.

Here is what this can look like in practice:

A retiree spends four nights in the hospital after a serious fall. The family calls the plan before discharge and is told the next level of care should be covered. What no one makes clear is that the hospital stay was recorded as observation status. After the patient moves to a skilled nursing facility, the family receives a bill for tens of thousands of dollars.

The question to ask before discharge is simple:

“Am I admitted as an inpatient, or am I here under observation status?”

Ask the doctor, the hospital case manager, and the discharge planner. Ask for the answer in writing. Medicare specifically advises patients and caregivers to ask each day whether the patient is inpatient or outpatient.

Rule 2: The IRMAA Trap — Past Income Can Raise Today’s Premiums

Medicare does not always price your premiums based on what you earn right now.

For 2026, Social Security generally uses tax return data from 2024 to determine whether you owe an Income-Related Monthly Adjustment Amount, known as IRMAA. That means a one-time financial event from two years ago — such as selling property, converting a traditional IRA to a Roth IRA, taking a large retirement account withdrawal, or realizing capital gains — can raise your Medicare premiums now.

For 2026, the standard Medicare Part B premium is $202.90 per month. Higher-income beneficiaries pay more based on their modified adjusted gross income. For individual filers, the 2026 Part B premium rises as follows:

| 2024 Individual MAGI | 2026 Monthly Part B Premium |

|---|---|

| $109,000 or less | $202.90 |

| $109,001 – $137,000 | $284.10 |

| $137,001 – $171,000 | $405.80 |

| $171,001 – $205,000 | $527.50 |

| $205,001 – under $500,000 | $649.20 |

| $500,000 or more | $689.90 |

Consider this example:

A retired homeowner with $68,000 in annual income sells a property and realizes $102,700 in taxable gain. Added together, that puts the person’s 2024 income at $170,700. In 2026, that income level can push the monthly Part B premium from $202.90 to $405.80 — an added $2,434.80 per year for Part B alone. If the person also has Part D coverage, an additional Part D IRMAA may apply.

There is one possible remedy many retirees never hear about: Form SSA-44.

Form SSA-44 allows you to request a new IRMAA decision if your income went down because of certain life-changing events, such as marriage, divorce, death of a spouse, work stoppage, work reduction, loss of certain income-producing property, loss of pension income, or certain employer settlement payments. It does not automatically erase the effect of a capital gain by itself, but it can help when a qualifying event reduced your ongoing income.

Rule 3: Prior Authorization Has New Timelines — But Denials Still Happen

Prior authorization continues to be one of the biggest pain points in Medicare Advantage.

Starting January 1, 2026, impacted payers, including Medicare Advantage plans, must send prior authorization decisions for medical items and services within 72 hours for urgent requests and 7 calendar days for standard requests. That is a meaningful improvement.

But faster deadlines do not mean automatic approval.

If your plan denies care, delays care, or refuses to cover a service, you still need to know how to act. Medicare Advantage appeals have multiple levels, and the first level is called a reconsideration. If waiting for the standard decision could seriously harm your health, you can request a fast or expedited appeal. In qualifying cases, the plan must respond within 72 hours.

If you receive a denial:

Request the appeal immediately. Ask your doctor to provide written medical support. Request expedited review if the delay could affect your recovery, health, or ability to regain function. Keep copies of every letter, fax, portal message, and phone call record.

Do not assume the plan will guide you through the process. The appeal rights exist, but you must use them.

Rule 4: The Part D Drug Cap Helps — But Not Everyone Benefits Equally

The prescription drug rule is one of the most important Medicare changes for people with high medication costs.

In 2026, annual out-of-pocket costs for covered Medicare Part D drugs are capped at $2,100. Once you reach that limit, you pay no additional copayment or coinsurance for covered Part D drugs for the rest of the calendar year. The original $2,000 cap began in 2025 and was indexed to $2,100 for 2026.

For retirees taking expensive brand-name or specialty medications, this can be a major financial relief.

The asterisk is that the cap may not help people whose annual drug costs are already low. If most of your prescriptions are inexpensive generics and your yearly drug spending is far below the cap, you may never reach the point where the protection applies.

There are also other costs to watch. In 2026, many Part D enrollees face deductibles, coinsurance, and formulary changes. KFF reports that most Part D enrollees are in plans with either the standard $615 deductible or a partial deductible, and the use of coinsurance has increased in Medicare Advantage drug plan formularies.

The practical move is simple: compare your actual prescriptions, pharmacy, deductible, premium, and copays every year. Do not choose a Part D or Medicare Advantage drug plan based only on the monthly premium.

Rule 5: Medicare Advantage Dental Benefits Can Change Quietly

Dental coverage is one of the most attractive features of many Medicare Advantage plans. But it is also one of the most misunderstood.

Original Medicare generally does not cover routine dental care. Medicare Advantage plans may offer dental, vision, hearing, and other extra benefits, but the scope of those benefits varies by plan. In 2026, nearly all individual Medicare Advantage plans offer some dental benefit, but the details can differ significantly. Some benefits may cover only preventive care, while others may include more comprehensive services subject to annual dollar limits, coinsurance, networks, and procedure-specific rules.

That means a procedure that looked affordable last year may cost more this year if the plan changed its benefit design, network, reimbursement rules, or annual allowance.

Before any major dental work, ask for three things:

- A written treatment plan from the dentist.

- A pre-treatment estimate or coverage confirmation from the plan.

- Your 2026 Evidence of Coverage document.

Your Evidence of Coverage explains what your plan covers, what you pay, and what changed. Medicare says plans send this document each year, usually in the fall, and beneficiaries should review it to decide whether the plan still meets their needs.

The surprise bill from one dental procedure can easily exceed what you expected to save by choosing a plan with “included” dental benefits.

Why These Problems Keep Happening

Most retirees do not discover these rules because they failed to pay attention. They discover them late because Medicare is complicated, Medicare Advantage plans vary, and the most important details are often buried in notices, plan documents, and billing classifications.

A hospital status label can determine whether skilled nursing care is covered. A tax return from two years ago can raise today’s premium. A prior authorization denial can delay care unless you appeal. A drug cap can help some retirees while leaving others exposed to deductibles and coinsurance. A dental benefit can look generous until the Evidence of Coverage shows the limits.

You paid into Medicare for decades. But the coverage you earned still comes with rules, exceptions, and cost-sharing responsibilities that can affect your retirement budget.

Knowing where the traps are is the first step toward avoiding them.

How Assureline Insurance Can Help

At Assureline Insurance, we help Medicare beneficiaries in Orlando and across Florida understand their coverage before a bill becomes a problem.

Our licensed advisors can help you:

- Review your current Medicare Advantage plan in light of 2026 changes.

- Compare Medicare Advantage, Part D, and Medicare Supplement options.

- Understand whether Form SSA-44 may apply to an IRMAA situation.

- Review prescription drug costs, deductibles, and pharmacy options.

- Explain your rights after a prior authorization denial.

- Evaluate whether your dental, vision, and hearing benefits still meet your needs.

Medicare decisions are too important to leave to guesswork.

Call Assureline Insurance today at (407) 502-0203.